When "Private Credit" Doesn't Mean Fixed Income

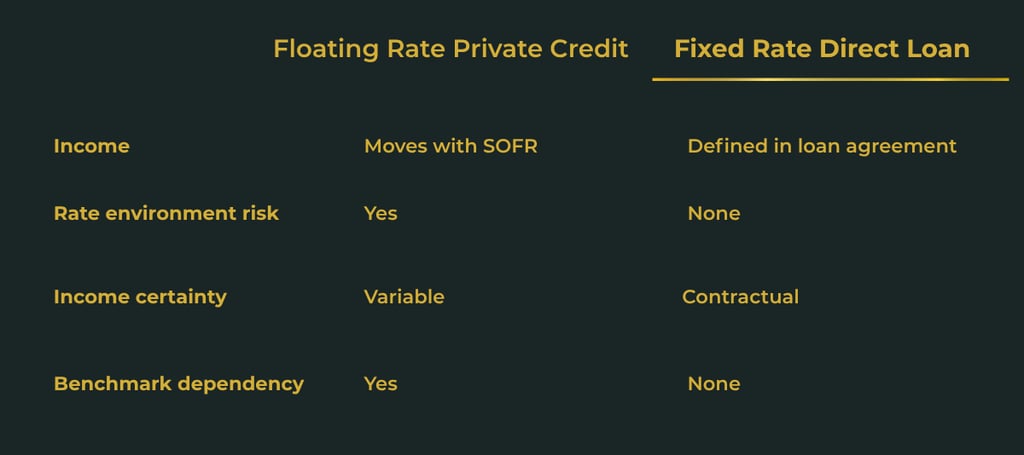

Private credit has reshaped fixed income but most of it floats.

FIXED INCOMESTRUCTURE

Accredited investors only. All inquiries by written request only.

©2026 Wellcome Capital Consulting Inc. | Incorporated in Alberta, Canada. All rights reserved.

Content for informational purposes only. Not legal, tax, or investment advice • Privacy Policy

YieldShield Aurum is the branded name used by Wellcome Capital for a direct bilateral loan agreement between an accredited investor and the borrower counterparty, supported by a principal protection insurance policy issued directly to the investor by an assigned insurance carrier. The borrower is an independent Nevis-registered private wealth-lending platform. Monthly interest is paid directly by the borrower. Principal protection is provided by the investor's insurance carrier under the terms of the policy. Wellcome Capital acts solely as marketing and introduction partner. It is not a counterparty to the loan or the insurance policy, and bears no liability for capital, interest or insurance obligations. All contractual obligations rest with the borrower and the assigned insurance carrier respectively. For informational purposes only. Not investment advice. For accredited investors only